Closing a financial year

A step by step guide to closeing a financial year in Analog TLDR: At the end of the year there are several steps to do before closing is possible. Below are some pointers to keep in mind: - Check “lager beholdning”, insert the value of clips that have been bought, but not yet used. This should be inserted in the konto: (hensat til ubrugte klip) - If the numbers do not match, check previous months. Check if there are things that are not bookkept. - When things are registered in 2020, but paid in 2021, these should change as we use “kontakt princippet”. - If we have outstanding money, then money should be bookkept as “andre tilgodehavende”, and deducted when it receives our account - Do as economic recommends at last when closing the year - do not “clear all”.

- Step 1 - Checking all bank accounts and Pleo

- Step 2 - Making sure we bookkept our accounts correctly

- Step 3 - Our assets, unused clipcards and debt

- Step 4 - Close it

Step 1 - Checking all bank accounts and Pleo

The first thing to do is to check that all transactions from bank accounts and pleo are bookkept in Economic.

In other words. Check the "bankafstemning" in economic for floating expenses. No floating transations in "bankafstemning" is allowed. Sometimes it will have the same line twice. You should make sure that every transation is unique.

- Danske Bank - Drift - sammenlign ultimosaldo i economic med bankens ultimosaldo (per 30/06)

- Danske Bank - Terminal - sammenlign ultimosaldo i economic med bankens ultimosaldo (per 30/06)

- Danske Bank - Cash Reserve - sammenlign ultimosaldo i economic med bankens ultimosaldo (per 30/06)

- Danske Bank - MobilePay - sammenlign ultimosaldo i economic med bankens ultimosaldo (per 30/06)

- Pleo Wallet sammenlign ultimosaldo i economic med Pleos ultimosaldo (per 30/06)

When every account shows the same amount (per 30/06). That means that it is very likely, that you have every transation in your "regnskab". That is a good sign.

Remeber! This is the last chance to make sure that all income has been bookkept correctly. Be aware of Terminal and Mobile pay. The income being reported correct is your responsibility.

Now we go on to step 2. Checking that our internal accounts are correct.

Step 2 - Making sure we bookkept our accounts correctly

Say we have bookkept a travel expense as a Board meeting. Then this will show up incorectly when we make the report.

To avoide mistakes like this. We go through the report and check that expenses are marked correctly. Fees from the bank is a good example of something that is usally bookkept wrong.

Here we are mostly looking at what we have for expenses.

In step 3 we look at our assets

Step 3 - Our assets, unused clipcards and debt

Here we are focused and capturing how analogs finances look in the bigger picture. We want to know how much of our money is tied up in clipcards and stock.

Clipcards:

We have an obligation to give people money back on their clipcards up to 3 years after they bought them. Therefore we need to adjust how much of our asserts are tied up in clipcards. Even though the money is in the bank. We cannot see it as our money until the clipcards have expired. ( In a sense expired clipcards can still be used. But we do not have an obligation to refund them).

We use this sql code to get the info on how much money is tied up in clipcards from the day we close the year (30/06) and three years back.

The date xxxx-06-30 00:00 should be replaced with the year you are closing the finicial year minus 3 years.

Say 2028-06-30 00:00 in 2031-06-30 00:00

SELECT

YEAR(t.DateCreated) AS 'Purchase Year',

p.Id as 'ProductId',

p.Name AS 'Product',

Count(t.Id) AS 'Unused tickets',

(ph.Price / ph.NumberOfTickets) AS 'Per ticket incl moms', -- Product price as the time of purchase

(ph.Price / ph.NumberOfTickets) * COUNT(t.Id) AS 'Subtotal incl moms' -- Subtotal of unused tickets with purchase price

FROM

Tickets t

INNER JOIN Purchases ph ON

ph.Id = t.Purchase_Id

INNER JOIN Products p ON

t.ProductId = p.Id

WHERE

ph.Completed = 1 -- Only look at completed Purchases

AND t.IsUsed = 0 -- and unused tickets

AND ph.DateCreated > 'XXXX-06-30 00:00' -- fromDate exclusive (only look at unused tickets after this date)

GROUP BY

p.Id,

p.Name,

YEAR(t.DateCreated),

(ph.Price / ph.NumberOfTickets)

ORDER BY

YEAR(t.DateCreated)Danish for what to do (Sorry)

- Ubrugte kaffeklip. Ubrugte kaffeklip opgøres og reguleres på lignende vis som med regulering af varelager. Analog er forpligtet til at tilbagebetale ubrugte kaffeklippekort op til 3 år efter købsdatoen, dv.s. lukkes regnskabet for 2020, tælles ubrugte kaffeklip fra 2017 med.

- Kør et dataudtræk fra AnalogIO’s AppSalg database : https://github.com/AnalogIO/analog-core/blob/develop/utils/db_scripts/unusedclipcards-by-year-and-purchase-price.sql og udregn det samlede beløb.

- Beregn differencen mellem tidligere konto 6952 Ubrugte kaffeklip saldo og det nye beløb af ubrugte kaffeklip. Differencen bogføres med 6952 Ubrugte kaffeklip som konto og 1011 App indtæger som modkonto.

Varelager:

- Varelager. Tæl Analogs varelager op for varer af en væsentlig værdi fx kaffe, chai, plantemælk. Mindre ting som fx rørepinde kan udelades. Varelagerets værdi beregnes udfra indkøbsprisen inkl. Moms.

- Dernæst skal varelager reguleres. Konto 5520 Varelager vil allerede have en saldo fra tidligere regnskabsår. Differencen mellem den eksisterende varelager saldo og det optalte varelager, bogføres på konto 5520 Varelager med 1330 Regulering af varelager som modkonto.

- Eksempelvis hvis konto 5520 Varelager har en saldo på 3.000 kr. og det optalte varelager er på 5.000 kr., laves der et finansbilag på 2.000 kr. (debet).

Debt:

If analog has debt, then it might make sense to add it to the bookkeeping. This will make it visual. And when you present the final report, then it will give a better understanding of Analog. We have done this in 2020-2021 with Punktafgift. Because we had money we owed. That they at that time had not asked for yet. We wanted to show it in the report. So the amount in the bank did not look like a profit, when it in reality was not ours.

This is best practise.

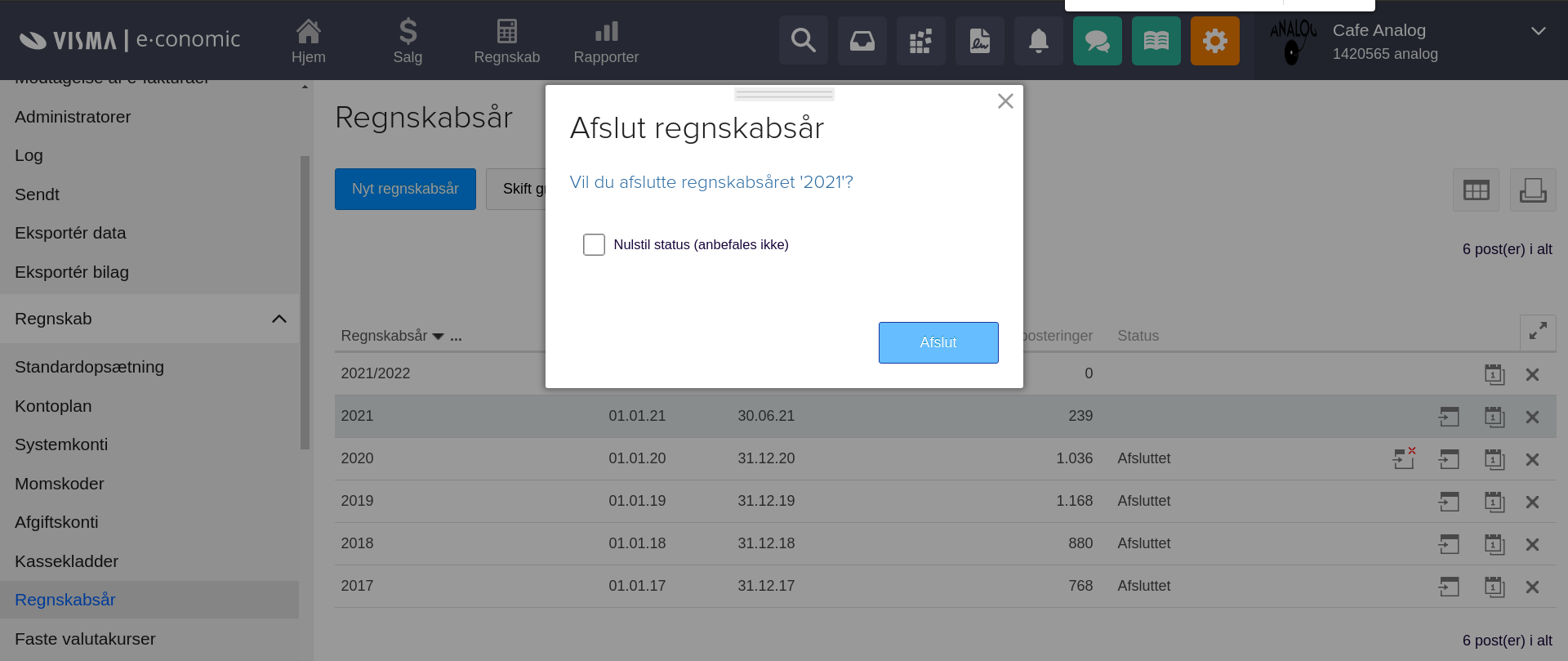

Step 4 - Close it

Before you do this, double check with experts, other people, etc. There is no exact deadline, so please make sure you do it right rather than quickly. Note: when you do it, DO NOT X THE BOX as shown below.